What to consider when your super balance is going up and down

Seeing your super account balance fluctuate can be uncomfortable but it’s not uncommon. That’s why we say ups and downs are a normal part of financial markets.

With plenty of worrying news headlines out there, it can be tempting to make sudden changes to your super. But history has shown that the most important thing you can do though is to remain patient and maintain a long-term perspective.

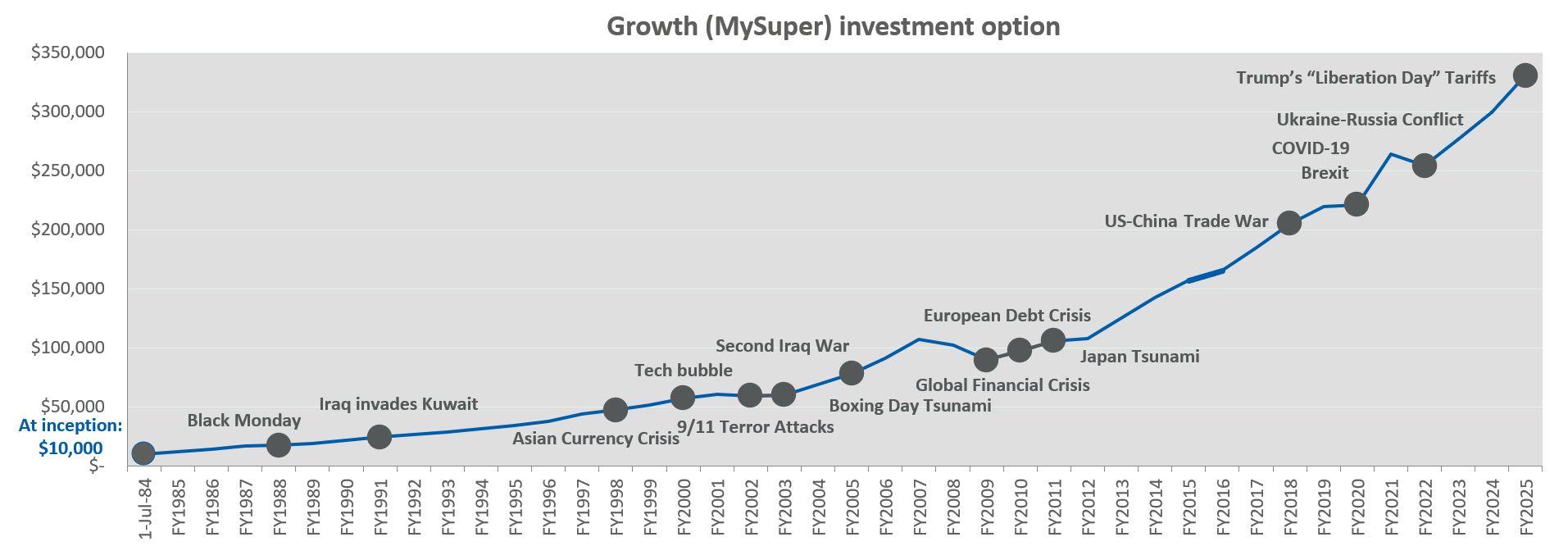

Investment markets do tend to recover over time. When you look back, you can often wonder what all the fuss was about. For example, how many of these major market events below do you remember?

From 1 July 1984 to 30 June 2025. This example is for illustration purposes only. Balances have been calculated using financial year investment returns compounding annually with no additional contributions and does not take into account the impact of inflation. The crediting rate is based on investment returns minus investment fees and costs, transaction costs and investment-related taxes and until 31 January 2020, the percentage-based administration fee. Excludes fees and costs that are deducted directly from members’ accounts. Past performance is not a reliable indicator of future performance.

More importantly, this chart shows that over the long term, the best course of action was to simply stay invested.

Believe it or not, this type of information doesn’t get many clicks or sell many newspapers!

How your decisions can affect your account balance

The decisions you make during a period of market ups and downs can have a lasting impact on your retirement.

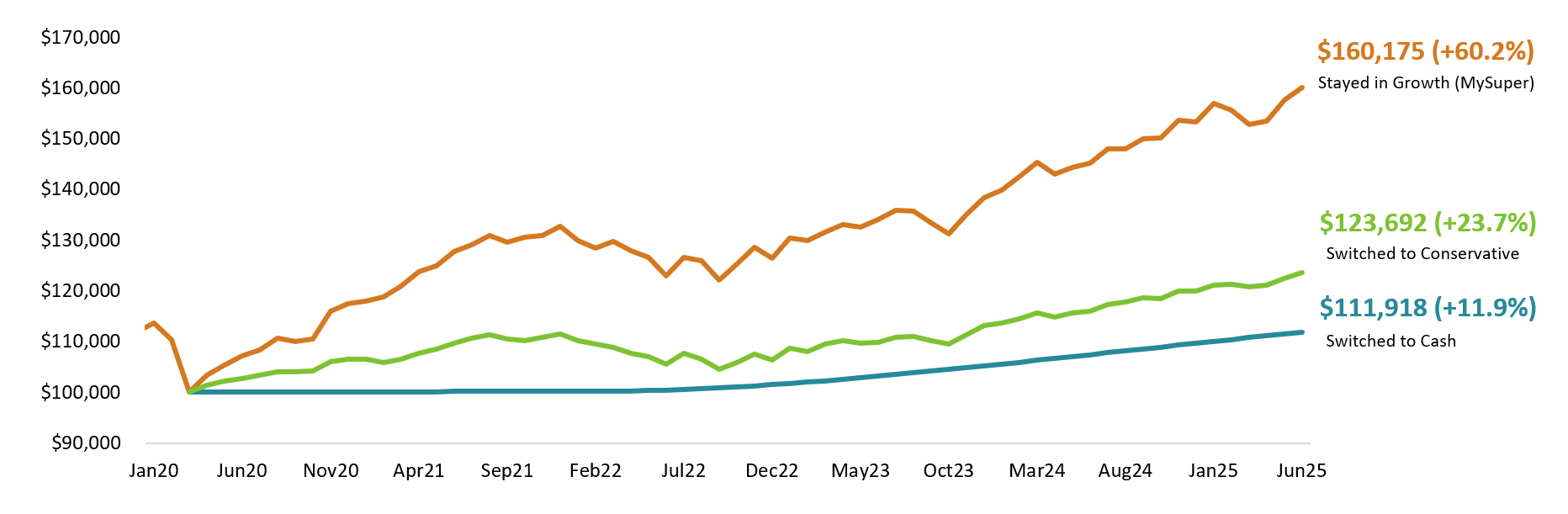

Take for example Amanda. She was invested in the Growth (MySuper) investment option and was concerned when she saw her account balance drop during a period of market volatility.

These figures are for illustration purposes only. The crediting rate is based on investment returns minus investment fees and costs, transaction costs and investment-related taxes and until 31 January 2020, the percentage-based administration fee. Excludes fees and costs that are deducted directly from members’ accounts. Calculations are based on historical crediting rates from 31 December 2019 to 30 June 2025, switching on 31 March 2020 with a super account balance of $100,000. Past performance is not a reliable indicator of future performance.

As the chart above shows, making a hasty decision that doesn’t take your long-term goals into account, can be risky and potentially add up over time.

It’s very difficult to get the timing right. You might end up switching too early or too late. Missing just a few days of a rebound can have a large impact on your account balance when you look back a few years later.

What if I don’t have time to ride out the market ups and downs?

While members approaching retirement may need to consider a more conservative approach, most have time to ride out any ups and downs. Don't forget that even once you retire, you may still need to consider growth assets, like shares, in your investment option.

Whatever your situation, ensuring you stay focused on your plan is the best way to ensure you meet your long term goals.

If you're thinking about changing investments based on what's happening in the investment markets, it’s a good idea to get advice first.

Help and resources

Contact us

Do you still have questions or want to know more? We're here to help.

The team is currently experiencing a high volume of calls, which is resulting in longer wait times than usual.

Learn about investments

Read about the different investment options we offer, plus other important information in our Investment guide.

Understanding risk

Learn more in a comprehensive factsheet that can help you understand the different types of risk that can affect your super.