Retirement

The Age Pension

When you receive retirement income from your super, you may still be eligible for the government Age Pension.

Read more...For many, retirement income comes from a few different places.

See how super, the Age Pension and other income options can fit together.

Watch the video to learn more.

Read the transcript

Hi, I'm Jeff Wallens, Senior Education Specialist at CBUS.

I've spent 25 years in super helping people make sense of what they've got and what they can do with it. This is 'Straight Talk'.

We break down the parts of super that matter in plain language so you know what to do next.

When you start thinking about slowing down with work, one question comes up pretty quickly. How much will I actually have to live on?

Your super plays a part, but it doesn't have to carry everything, especially once you reach Age Pension age, which is 67.

In this video, we'll walk through three income sources you can use as you wind down or stop work. You'll probably know the first two, but the third one might surprise you.

Combine them and you can have more to work with than you think. First up, the Age Pension.

For some people it becomes their main income, for others it helps top things up. Depending on your situation, it could be as much as this each year.

Here's the part most people don't realise.

Some Australians miss out on thousands of dollars simply because they apply too late. Payments only start from when you apply, they're not backdated.

That's why timing matters.

Wait, and you don't just delay the payments, you miss out on them entirely. Even a few months can make a difference. Over a year it can add up to thousands.

Knowing when to apply can have a real impact on what you end up with.

In fact, research showed that one in three Australians wait more than a year to claim. Some miss out for even longer.

More than one in two Australians aged over 67 qualify for either a full age pension or a part payment.

By age 80, that rises to more than 75%.

For many, it becomes a key part of their income later on, and you don't need to be retired to receive it.

To qualify for the Age Pension, there's a few things to tick off. You need to be 67 or older.

You need to be an Australian resident for at least 10 years, including five continuous years.

Centrelink looks at what you earn and what you own to work out if you qualify and how much you may receive.

Income can include wages, rental income and deemed income from your financial assets, including super.

That's income Centrelink assumes your savings or investments pay you based on set rates, even if they're not earning that much.

Some pensions, annuities and overseas income may also be included.

Assets include things you own, such as cars, home contents, investment properties and savings. Your super counts once you reach Age Pension age.

The home you live in usually is not included in the assets test.

Different limits apply depending on whether you're single or part of a couple and whether you own your home. These details might seem small, but they can shift your outcome.

What you receive depends on how everything is assessed together. It's worth looking at the full picture, not just one part of it.

Your eligibility can change over time even if you don't qualify straight away, so it's important to look again later.

You can check the details on the Services Australia website or use the CBUS Age Pension calculator to get an estimate.

Now let's talk about super. Some people retire with enough to cover most of their expenses. However, for most CBUS members, that's not the case.

The good news is your super doesn't have to do all the heavy lifting. It works alongside other income. This is where things start to come together.

When you look at each income source on its own, it can feel like it won't go far, but combine them and you start to see what's possible.

For example, if you had $150,000 in super, this could provide you with this much income each year.

In this situation, super plays a role, but it doesn't have to be the main player.

The third option is something fewer people know about. It's called the Centrelink Home Equity Access Scheme.

If you own your home, it lets you turn part of its value into an income stream.

For example, a couple with a home worth $800,000 could receive this much each year. So how does it work?

It's a Government scheme that lets Australians of Age Pension age receive non-taxable fortnightly loan payments from Centrelink.

And you can take that income as a fortnightly payment, a lump sum or a mix of both. It's a loan secured against your home and needs to be repaid later with interest.

This interest compounds each fortnight on the loan balance until it's repaid in full. Over time the amount owing can grow.

You can choose to pay the interest as you go or leave it to be repaid later when the home is sold or your estate settles upon your death.

There's also a no negative equity guarantee, which means you or your estate won't have to repay more than the home's market value.

To qualify, you need to be 67 or older and eligible for payments such as the Age Pension, Carer Payment or Disability Support Pension.

Even if your Age Pension payment is $0 because your income and assets are over the thresholds, you might still qualify. If you rent, there's support available.

It's called Rent Assistance.

If you pay rent and receive certain Centrelink payments, you'll get this automatically. No separate claim is needed.

Services Australia checks your eligibility when you apply for payments or update your living details.

If you're eligible, you may be asked to complete a rent certificate or provide a tenancy agreement. When you combine these income sources, this is what it could look like.

This is where things start to shift. It's not just about one income stream, it's about how they work together. Seeing it like that makes it a lot clearer.

Yeah, there's a bit to take in here, but you don't have to figure it out on your own.

We run seminars and webinars where our Education team breaks this down in a clear, practical way. They're easy to follow and included as part of your membership.

You can also listen to our podcast CBUS Super Shift, where we talk about super and preparing for life after work.

Or head to the CBUS website, where you'll find tools and guides to help you plan your next steps. And if you'd rather talk it through, give the CBUS Advice team a call.

They'll chat about your options and help you see how it all fits together.

Once you do, you'll have a clearer picture of what your retirement could look like.

JobSeeker Payment

The JobSeeker Payment is financial help if you're between 22 and 67 and looking for work. It's also for when you're sick or injured and can't do your usual work for a short time. To get the JobSeeker Payment, you need to meet certain criteria, including income and assets tests.

Disability Support Pension

The Disability Support Pension is financial help if you have a physical, intellectual or psychiatric condition that's likely to last for more than 2 years, which stops you from working. There are criteria you need to meet if you claim this benefit.

Home Equity Access Scheme

The Home Equity Access Scheme (HEAS) lets Australians aged 67 or older receive non-taxable loan payments or a lump sum from Centrelink, using their Australian real estate as security.

A no negative equity guarantee applies, meaning you'll never owe Centrelink more than the value of the property secured against the loan.

The HEAS is available to those who qualify for the Age Pension or meet the qualifying rules but don't get any Age Pension, because their income or assets are over the thresholds. It can provide up to $67,000 per year for a couple, minus any Age Pension payments already being received.

You and your partner may be able to use the scheme in combination with other sources of retirement income.

Commonwealth Seniors Health Card

A Commonwealth Seniors Health Card is a concession card to get cheaper health care and some discounts if you are 67 or older and not receiving any Age Pension.

To get this card you need to meet some conditions, including an income test.

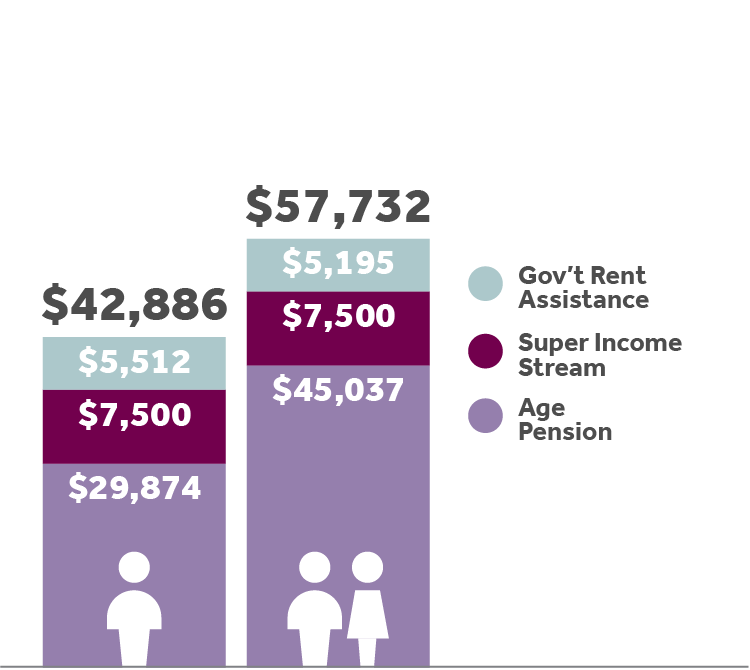

For a single person or a couple who are renting, you may be able to make up your income from a combination of:

Annual retirement income from 67:*

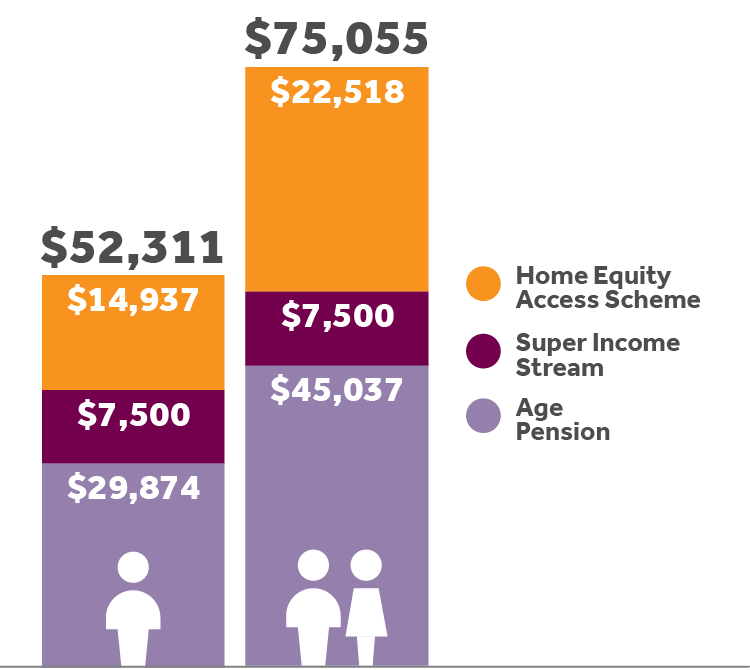

For a single person or a couple who own a home, you may be able to make up your income from a combination of:

Annual retirement income from 67:*

*Assumptions: